Just what is the requirement?

It is a new Canadian regulatory requirement about the information to be included on a client’s annual statement. It came into effect on January 1, 2026.

It applies in particular to segregated funds, mutual funds and exchange traded funds (ETFs).

This new requirement stems from a joint directive issued by the Canadian Council of Insurance Regulators and the Canadian Securities Administrators.

It is important to understand that there are no new fees.

The fees are staying the same (and this information has always been available to you). The difference is that the fees will now appear on the year-end statement and will be displayed separately and in a way that is easy to understand.

The goal of this new requirement

The new requirement has several goals, including:

Essential information

Enhancing your protection by ensuring that essential information is communicated to you, so you have a clear understanding of your investments.

Your rights and guarantees

Informing you of the rights tied to the guarantees in your segregated fund contract and the effects your decisions may have on those guarantees.

Transparency about the costs

Providing greater transparency about all costs associated with your investments so you can:

- better understand the fees you pay

- assess the impact of these fees on your investment portfolio’s return

- as a result, make informed decisions about your finances

What you should know about your year-end statement

Fund fees

The annual statement you receive will provide clear, detailed disclosure of the ongoing fees built into the management and operations of the segregated fund, expressed as a percentage and in dollar terms. It must include:

- The fund expense ratio (FER) for each fund owned

- The fund fees for your holdings shown in dollars

Total cost of your investments

There is also a new section that details the total cost for the year for the specific segregated funds you hold.

Performance and guarantees

New disclosures will also be provided regarding performance and contract guarantees.

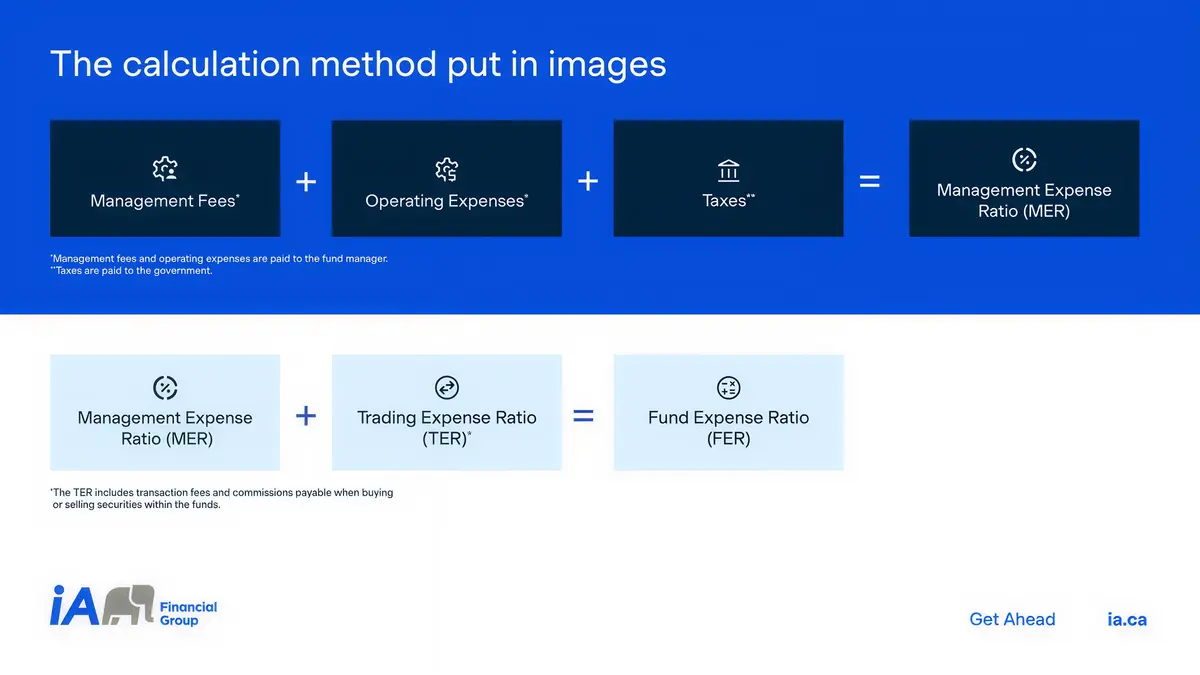

Understanding the different segregated fund fees

A segregated fund’s fee structure is much like that of a mutual fund, except for the protection and guarantee component, which delivers the unique benefits available only to segregated fund investors.

What are the fees used for?

The fees we collect are expressed in dollars on the statement. They are used to cover:

- The costs of managing the fund

- Operating expenses

- Protections and benefits

- The advisor’s guidance and wealth management expertise

Definitions of the ratios shown on the new statement

Management expense ratio (MER)

Trading Expense Ratio (TER)

Fund expense ratio (FER)

The different types of fees

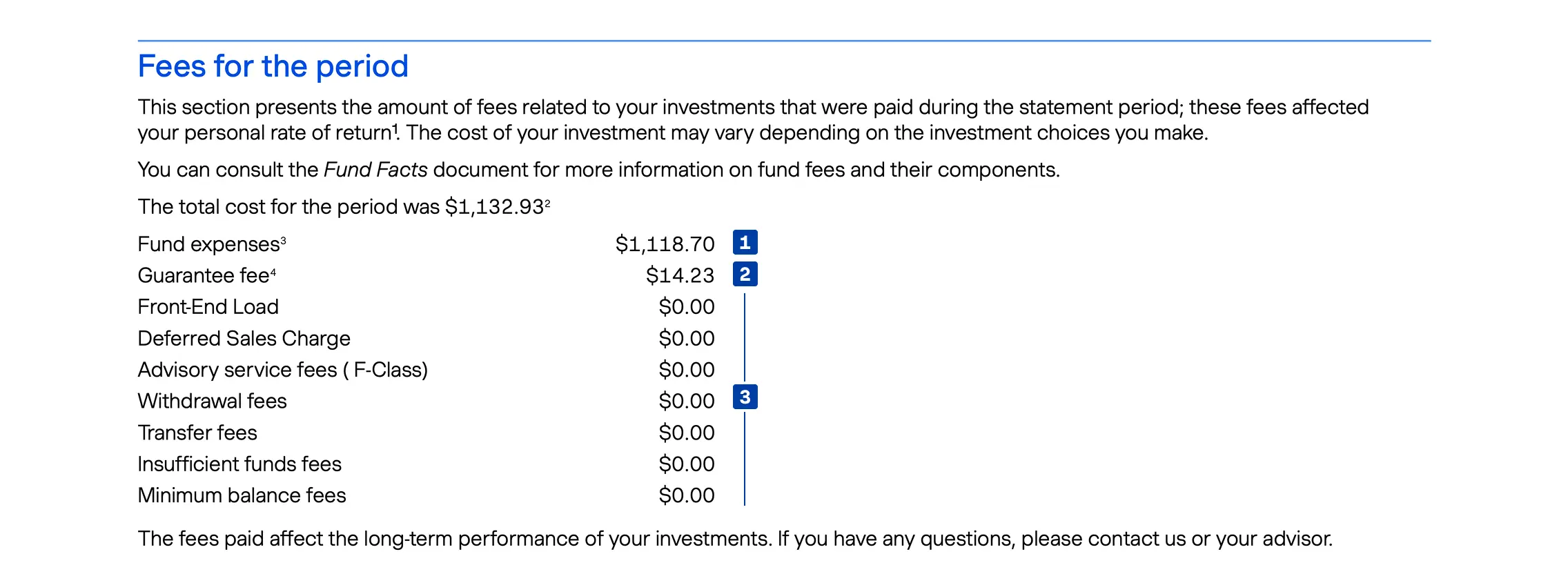

The Fees for the period section shows the list of fees paid during the year. These fees fall into three main categories.

1.Fund fees

2.Guarantee fees

3.Administration or service fees

1.Fund fees

These fees are in the indirect fee category. They are calculated daily and correspond to the fund fees in dollar terms.

You don’t pay them directly and you won’t receive an invoice. The fees are instead taken directly from the fund’s assets. This process lowers the fund’s daily unit value.

For more information, contact your financial advisor.

2.Guarantee fees

If this line appears on your statement, it means that you are paying these fees because you own one or more segregated funds in the following series:

- Series 75/100, Series 75/100 Prestige 300 and Series 75/100 Prestige 500

- Ecoflex Series 100/100 and Ecoflextra Series 75/100

- FORLIFE Series

They are calculated quarterly. You do not pay them directly. Instead iA recovers the amounts by redeeming units from your fund. For more details contact your financial advisor.

3.Administration or service fees

These fees fall under the direct fees category. They are billed on a recurring or occasional basis.

In all cases, you don’t receive a bill to pay. Instead, the fees are automatically withdrawn from the balance of the contract’s value.

For more information, contact your financial advisor.

Fees and personal rates of return

The percentage shown in the Personal rates of return section of your statement is the percentage after fees have been deducted; it therefore represents your net personal return (this has always been the case and is not new).

The value of an advisor and their guidance: much more than just returns!

The value of an advisor goes beyond the investment returns they help you generate. The guidance they provide and the peace of mind it brings are priceless.

Examples of your advisor’s added value:

- They help you build your wealth, manage risk and maximize your assets

- They can create a retirement plan tailored to your situation and set up an efficient withdrawal strategy when needed

- They offer savings and insurance solutions that are the best aligned with your needs and that cover all aspects and life events

- They can provide impartial and objective advice on your goals and prevent impulsive decisions that could lead to negative consequences.

Did you know?

Investors who work with an advisor for 15 years or more save 2.3 times more than their peers who do not.

Source: Claude Montmarquette and Alexandre Prud’homme, 2020

The real value of investing in a segregated fund and the advice that comes with it

iA ranks 1st in Canada for segregated fund sales and assets under management. Our comprehensive fund lineup offers investment options for all situations and economic cycles. What’s more, it can be adapted to each investor profile.

Segregated fund holders benefit from:

- Faster payment of proceeds upon death (about 10 business days)

- 3-in-1 protection (invested capital, resetting of investment gains¹ and creditor protection²)

- Cost savings associated with estate settlement (such as professional fees and probate fees³)

- The confidentiality afforded by naming a beneficiary, since settlement and transfer of the estate remain private and do not appear in the will

- The extensive expertise of an in house investment management team (iAGAM)

- A range of funds managed by renowned external managers and firms

- Enhanced potential returns and competitive management fees

Solutions and options for every budget

iA is committed to offering you competitive and high performing products. Over the years, we have evolved and enriched our product offering to meet a wide range of needs and budgets.

Prestige preferential pricing

Prestige preferential pricing, through the individual plan or the family grouping, can provide a substantial reduction in management fees, if you qualify.

Learn moreHigh interest savings account (HISA)

A high interest savings account can be a valuable addition to your investment strategy as it requires no minimum investment and lets you access your savings at any time. The HISA also includes all the benefits of segregated funds, such as quick settlement in the event of death and potential creditor protection.

Learn moreLow-cost investment options

There are index funds with lower management fees as well as funds where the commission is negotiated directly with the advisor (F-Class).

Ask your financial advisor about these products!

1. Available with Series 75/100, 100/100 and FORLIFE

2. Certain conditions apply.

3. Probate fees may vary based on the province of residence and personal situation of each client.

More than just savings products!

Your advisor’s job is to carry out a comprehensive review of your situation so that all aspects of your life are covered. Feel free to contact them.

I have an advisor

Sign in to the Client Space to access your information and connect with your advisor when needed.

Sign in to the Client SpaceI don't have an advisor

An advisor can help you navigate financial decisions and make informed choices.

Talk to an advisorNot sure you’ll remember everything?

Download the Quick Reference guide on management fees.

Download the Quick Reference guide